Creating Housing Affordability: Fixing Seattle to Solve a Global Crisis

5:30am. A tired hand, freshly jolted from a dream, fumbles around for the off switch to the screaming alarm clock. A young woman, two years removed from her college graduation, rolls out from under the covers into a world still hidden from the light of the morning sun. Though work doesn’t start until 8:00, she needs to leave by 6:20 if she wants to be on time. It’s days like this where she wonders what all went wrong; she has a degree, she has a salary paying her $3,000/month, but life hasn’t been at all what she was told to expect. Between car payments, gas, housing, utilities, and her student loans, she is spending around two-thirds of her income on bills. She wants to build a savings, but the $1,000 she has left is hardly enough to live on in any metropolis. What little savings she did have were recently wiped out by car maintenance, which has become more frequent in recent months. That’s what happens when you must commute 90 minutes each way on a daily basis. She moved to the suburbs despite her downtown city job in order to save money on housing costs, but those savings were replaced with the cost of gas, the wear on her car, and the stress that compounds with each new morning. Every day, she watches her dreams and opportunity slip further away. Every day, she helplessly carries on.

Cities around the globehave noticed an alarming trend; housing has become so unaffordable that it has wiped out the prospects of social and economic mobility for large numbers of residents. To afford the median home in Vancouver, B.C., Canada, requires 12.6 times the median annual income— $72,662 in 2015— meaning a starter home costs nearly $870,000 CAD (Kwan, S., 2019). The prosperity in cities like San Francisco, London, Vancouver, and Melbourne is truly unfathomable. Yet large swaths of their populations lack a place to call home, while even more people live on the precarious edge of displacement, eviction, and upheaval.

The aim of this paper is to analyze how the housing affordability crises observed in these cities compares to the one in the author’s hometown of Seattle, Washington, and how it can be best addressed. Seattle was the hottest housing market in the United States for much of the last decade, with the soaring cost of housing and living serving as the byproducts of the city’s transformation from a quirky, modest city isolated in the Pacific Northwest into a global hub of ideas, technology, and innovation. Through a combination of observing the experiences of cities even more entrenched in the struggle to remain affordable, identifying successful pursuits other cities have undertaken to create more equitable metropolises, and sifting through the deluge of research on this topic, this paper will attempt to promote policy solutions that, if successful in Seattle, can be applied globally. Crafted correctly, these policies can address social justice, economic mobility, and racial equity, while also preempting the negative impacts of future growth.

BACKGROUND

Housing prices across the globe have grown dramatically since the 2008 financial crash, particularly in cities. In most wealthy countries, the 2008 crash led to a massive restructuring of the economy, with nearly 9 million jobs being lost in the United States alone. During the recovery, the sectors that experienced the greatest job growth were primarily low-wage, namely the hospitality and service industries, with their growth fueled by the hiring of once-salaried workers from now-diminished industries. Many of these jobs arose to meet the needs of the information technology (IT) and financial industries that had experienced exorbitant income increases during the recovery (Green, K., 2017). With the concentration of IT and financial jobs in urban cores, the new economy pushed for a reversal in the long-trend of suburban flight. Between 2008-2017, the largest American cities accounted for 72% of all job growth, while many small communities still have unemployment below pre-recession levels. Between 2010-2014, only five U.S. metro areas accounted for over 50% of all new businesses created (Parilla, J., 2017). Across the globe, cities are becoming more populated, wealthier, and as a result, more expensive.

The world’s major cities now seem to all show the same trend: the clear class stratification between the well-paid elite, a surviving, but stressed middle class, and the precariously employed, wage-earning lower class. As the population and wealth of these cities have grown, the cities have not kept up with the rising demand for housing. With a lack of supply, housing prices, both for ownership and renting, have skyrocketed. Governments and economists consider a person “cost-burdened” when they are paying over 30% of their monthly income towards their housing. Across the United States, there are 19.7 million renting households making $35,000 or less per year; 86% of them are cost burdened. In 20 of the 25 largest metro areas in the United States, a median income renter would be cost-burdened if they paid the median rent (Salviati, C., 2018).

In the target city of this paper, Seattle, 47% of households are considered cost-burdened, with a greater percentage in the areas with a high concentration of renters. As many as 90% of households in Seattle’s University District are renters; 66% of them are cost-burdened. Between 2010 and 2015, the number of jobs in Seattle increased nearly twice as fast as the number of homes. Across that same time period, the average rent for a one-bedroom apartment increased 35 percent (Office of Planning and Community Development, 2016). The root causes of the affordability crisis are nearly identical in almost every plagued city, including a lack of new homes, little to no well-designed social housing (public housing designed to promote a positive feedback loop of ideal societal outcomes), and an exorbitant amount of political power in the homeowning and capital-controlling classes.

According to the famous theory put forth by psychologist Abraham Maslow, stable housing is one of the key needs that must be met in order to have a productive and joyous life. As of December 2018, there were at least 12,112 people in Seattle’s King County experiencing homelessness (DeWolf, Z., et al, 2018). In California’s Bay Area, estimates of their homeless population are between 19,000-25,000 (Kendall, M., 2018). According to the annual Point in Time Count, a mass survey to determine the number of people experiencing homelessness, 41% of respondents in King County

“If a community cannot provide housing to those who are the heart and soul of it — those who respond to disasters, provide health care, teach our kids and so on — then what kind of community is that to live in?” – Christine Gregoire, Former Governor of Washington

THE CAUSE AND EFFECTS OF OVERPRICED HOUSING

The 2008 Crash Leaves Its Mark

For much of the 20thCentury, the American populace was primarily composed of homeowners. Long considered the essential asset to building wealth, home ownership was the centerpiece of the American dream. The red front door, the verdant lawn, the white picket fence. While that may have more to do with a fabulous marketing campaign from the real estate and financial industries, it’s what the majority strove to achieve; never has this been more exemplified than in the run-up to the 2008 global financial crash. The pernicious hope that prosperity was a simple purchase and sale agreement away played directly into the hands of vicious predatory lenders, willing to qualify teachers making $40,000/yr. for a $600,000 home. The originating lenders were protected from the inevitable loan default; loans were sold to third-parties who would collect the debt in exchange for an upfront fee. These third-parties then cut up these loans into tiny fractions and paired them with the tiny fractions of thousands of other loans, before selling these new Frankenstein loans to someone else. The end-buyer was supposedly buying a very low-risk financial product. One homeowner might default on their loan, but because hundreds (or thousands) of people had miniscule ownership stakes in the loan, representing only a sliver of their portfolios, no one would feel that much pain. The only thing that could go wrong would be a system-wide failure.

In late 2006, global housing prices started to shake. After a half-decade of unprecedented growth in the real estate market, a wave of foreclosures across the United States precipitated coming disaster. An economy bolstered since 2001 by low-interest rates had begun to slow. The Federal Reserve decided to raise interest rates in order to cool inflation fueled by cheap credit. However, the Fed did not realize how much the economy had also been propped upon fraud, predation, and corruption. As rates rose and credit became harder to access, homeowners in possession of adjustable-rate mortgages (loans with rates that can change at the lender’s discretion) started seeing their monthly payments soar.

Many of these adjustable-rate mortgages were entered into as existing homeowners were encouraged to refinance their houses. Lenders advertised low-interest rates and pointed to the massive appreciation in housing since 2001. Lenders were seeking to make a pretty origination fee; homeowners were wooed by the equity in their assets. According to a report from the Federal Reserve, in 2005 alone, U.S. homeowners extracted $750 billion in equity from their homes (Greenspan, A., &Kennedy, J., 2007). This debt poured fuel on the fire, further heating an already burning economy… and leaving an even larger trail of destruction in its place.

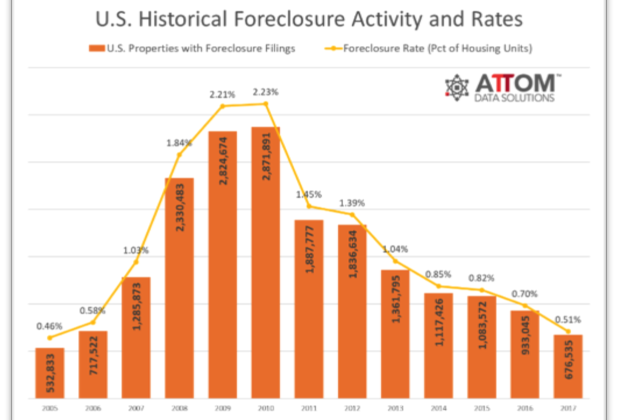

In 2005, there was a total of 532,833 foreclosures across the United States. In both 2008 and 2009, there were over 2,800,000. Between 2007 and 2012, a total of 13,010,332 foreclosures took place (Figure 1). $13 trillion of household wealth dissolved. At least 9 million jobs were lost, some permanently (Kalleberg, A., & Von Watcher, T., 2018). Retirement plans and pensions were wiped out. This historic collapse dramatically changed the face of everything it touched, especially the housing market. The white picket fence had been turned to sand.