MIZ Example: No Value Exchange, Just Higher Prices

I’ve been writing about the problems with Mandatory Inclusionary Zoning (MIZ) for a long time now. In short, MIZ is infeasible, inflationary, and most likely illegal. The idea of extracting money to pay for rent restricted housing might be a good political solution but it would add costs that would make some projects infeasible and when they did pencil, it would be because prices would have gone up to offset the financial impact. It’s worth taking a closer look at how the current MIZ creates feasibility problems that can only be improved when the price of housing goes up – if it can.

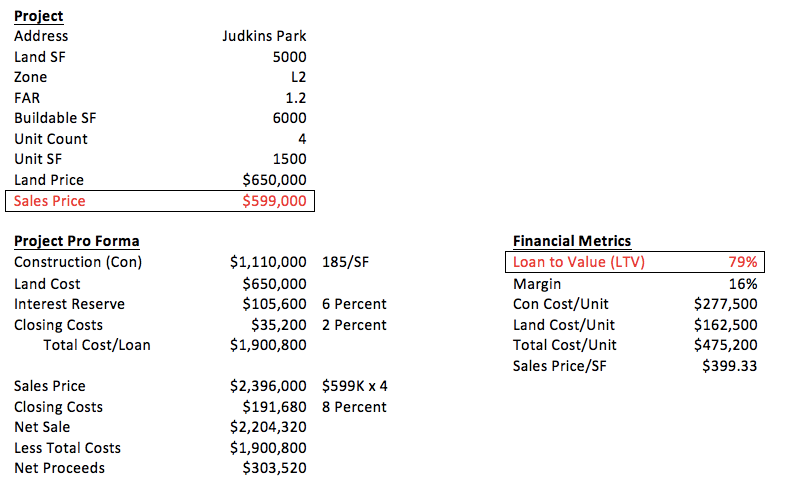

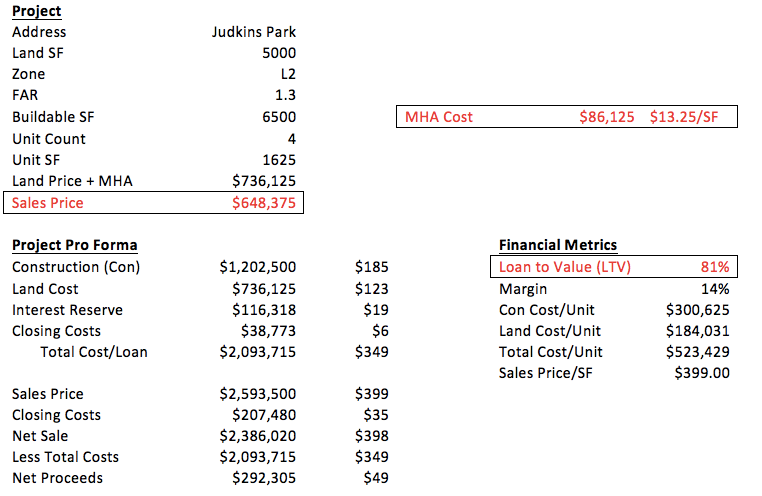

A 4 Unit Townhouse Project: Before MIZ

The example we have put together is a townhouse project in Judkins Park. Most of the assumptions are in the following table.

The most important number to watch on the table as an indicator of feasibility is the Loan to Value measure or LTV on the far right. Contrary to what some people might think or believe almost every development project in the city is built with borrowed money either from investors putting in cash with an expectation of a return payment or a bank that is charging interest. No matter where the money is coming from, there is always a measure of the debt to the value of the project.

In the case of multifamily housing projects financing over a period of years, this is usually called a Debt to Credit Ratio or a DCR and in townhouse or single-family projects an LTV. A DCR is usually expressed using decimals with an optimal DCR being around 1.20. Roughly, this means that for every dollar borrowed, the project must produce at least $1.20 in income to cover the operations of the project and the debt service. In a for sale product, the LTV is an indictor of the coverage of the borrowed money compared to the anticipated value of the sale at closing. An optimal LTV would be about 80 percent. As the LTV goes higher, lenders and investors are unlikely to provide funding, since for them it is a measure of risk. The lower the LTV, the more likely the project will produce the required return on investment.

This project currently is meeting that minimal expectation with a unit sale price of $599,000. It’s important to understand that the lender or investor also sets the price based on what they believe the market will bear. If the LTV is 65 percent, but the price of the product seems way too high, the lender will push back and demand a lower sales price. In other words, the bank might not believe that this particular product, in this neighborhood will get $599,000. If that’s the case the project won’t happen. Other options are to find ways to lower costs.

Every development project goes through this feasibility phase in which costs, the market price, and the potential return and risk are all vetted and discussed. Every party in the transaction wants to be sure that at the end of the 12-month period, they’ll be able to walk away with a return on the investment that justifies the risk. If there isn’t any confidence in this, the project won’t get beyond this phase, the land won’t be purchased, contracts won’t be put out for bid, and whatever sits on that 5000SF lot will remain.

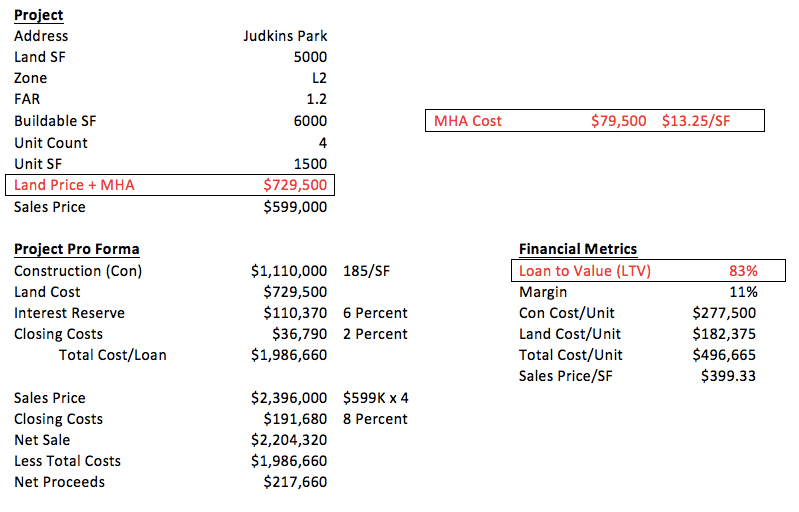

A 4 Unit Townhouse Project: After MIZ

So what happens to this project when MIZ is imposed?

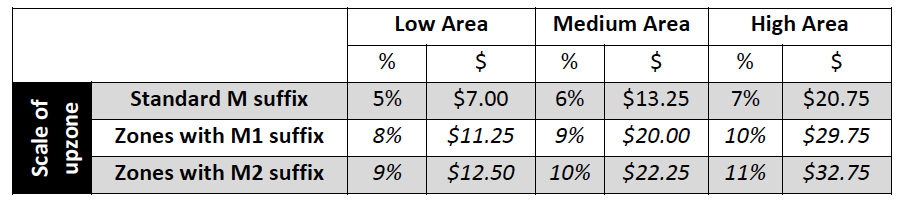

The assumptions for this project includes that it is in an area designated as “Low” under the MIZ requirements imposed by the Mayor’s Mandatory Housing Affordability (MHA) legislation. The “Low” designation indicates areas deemed to have low rents or lower priced housing. However, after the Mayor got together with Councilmember Lisa Herbold several weeks ago to devise a Displacement Index that would boost the fees and inclusion rates in those areas (supposedly to avoid “displacement” created by new housing, this project is now in a “Medium” area.

The Medium-MHA geographic area is expanded to include formerly Low-MHA areas: North Beacon Hill, North Rainier, and Columbia City, Northgate, and Crown Hill. Development in these areas will be subject to MHA Medium amounts that range from 6% to 10%. These changes increase the area citywide where high and medium MHA payment and performance amounts apply.

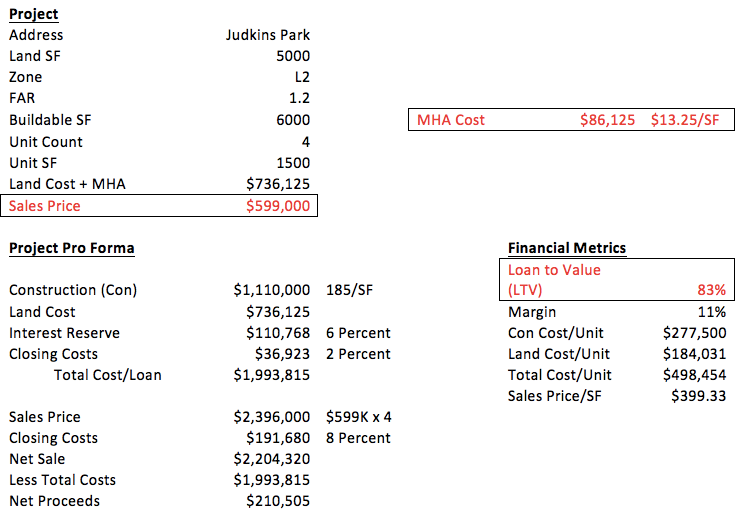

So what happens to the project when it pays $13.25 a square foot for the in lieu fee (and remember builders pay for additional square feet whether they use it or not, and here that’s 500 SF or about $6000)?

It’s important to note that the builder said this about the additional square footage that comes along with the MHA program:

I would not build the additional [square footage] granted by MHA in this project. It doesn’t make financial sense to build the additional SF. You would have to build a fourth floor and the market doesn’t like fourth floors and wont pay the normal sales per SF for a 4th floor.

Also keep in mind that the additional construction costs for the fourth floor if it was built would also add costs to the project. I’m not going to do the math all the way through here, but building the additional square footage would add to the sales price of the unit and to the loan amount, but there would also be some additional expense. However, the builder of this project says people (the market is people after all) aren’t buying 4 story townhouses.

But just as important, notice the change in the LTV; it’s now at 80 percent. That change means banks or investors won’t provide the needed capital for the project, so the project won’t happen. What the builder can do is find additional sources of funding to cover the new costs. He could also find a way to lower construction costs or he could find another lender willing to take more risk.

But what is the most likely scenario? The price for the units will increase, provided people looking for homes are willing to pay more for this product in this neighborhood.

There you have it. Fees imposed will either slow production by putting projects out of feasibility or prices for housing will go up to absorb the additional costs, provided people can and will pay the higher prices.

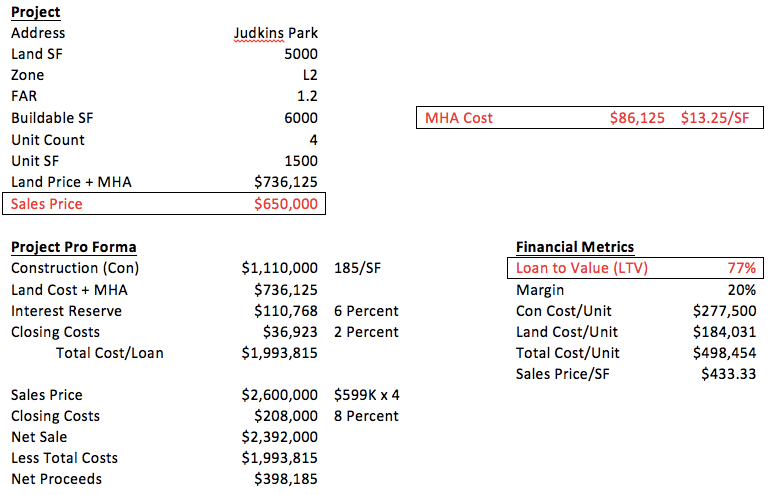

Let’s look at one more possibility. What if the builder used the additional 500 square feet granted for the fees being charged?

The additional “bonus” square footage offered by the City’s MIZ proposal doesn’t help very much even if it can be used on the site and without the price boost, actually lowers the per square foot sales price ($399) if the price stays the same, $599,000. Instead, in this case, those extra square feet have to be offset with an additional $50,000 on the price and the LTV is still too high. As I’ve said before, the City’s MIZ program is not a value exchange program but an exaction. What happens in this example is either nothing when the project doesn’t pencil, the price of the housing goes up to make it work, and even when the additional FAR is factored in, it doesn’t produce much vale for the hassles and costs associated with it.

There a many other lenses to view this example, including the City’s argument and assumption that the price of the land would go down exactly as much as the fee. We can argue about that all day, but what I hear from people who make housing is that this simply won’t happen, and if it did, the owner of the land with a single-family house in this zone would just sell it to someone who wants to live in it, not for development. That means a loss to the market of 4 houses; and, importantly, $0 in fees for the City.

Finally, this example is for discussion. Each and every project will have different up sides and down sides. But what we know doesn’t help production is additional costs and process. What will happen isn’t so much that builders will discover this impact as they build, but the new fees will get baked in essentially to production. Housing production will go on once prices go up enough to simply include the fee in the cost of doing business. This same scenario will play out with other kinds of housing too, including apartments. That’s not a good solution for people who say we’re having an affordability crisis in housing. It’s time to reconsider this intervention and exchange it for one that would have a beneficial impact on price.

{kind=link}