Rent Control? What About Cost Control?

Yesterday, 43rd Legislative District Candidate Jess Spear made a case for rent control. We’ve already explained why rent control is inflationary, and a bad idea whether it is imposed by the City Council or a Roman Emperor. But how fast are rents rising? And what will make them go higher? What effect would rent control have if it took effect?

This post relies on data put together by real estate data guru Mike Scott of Dupree + Scott. The data I am citing was created for the Downtown Seattle Association (DSA) and for articles in the Rental Housing Association (RHA) newsletter.

Some people out there will rule this data out of bounds because it’s biased. That’s fine. I’ve been transparent where it came from. I am happy to see other data if it exists. My point is to inject some data into a largely emotional discussion about rents.

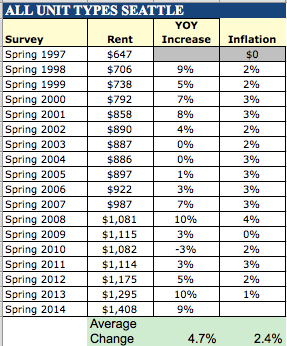

According to figures from the DSA, rents in Seattle increased about 5 percent per year on average since 1997. In some years it didn’t go up at all. Other years rent went down. Yes, rents go down.

Keep in mind that the increase in an individual’s rent often doesn’t increase annually; instead, it often has periodic jumps. For example, if I pay $900 a month in rent, my rent might not go up for three years; then it might increase by $150. That’s a one-time increase of 15 percent, but during my time in the apartment it’s about 5 percent per year, consistent with the market.

It still might sting. But my wages and prices for everything else probably changed, too. For someone who just lost a job, getting hit with that rent increase adds insult to injury. For others who got cost of living adjustments over the same time, it might be manageable. It all depends. I am not taking away from the challenges people face, but I am also trying to point out, that on the whole, rents are keeping pace with most other prices and wages.

According to Mike Scott, in the RHA newsletter, rents tracked up at just over 3 percent in King County, roughly the same rate as inflation if we discount 2009, which had negative inflation. But what about operating expenses faced by landlords?

Between 2000 and 2013 collected [rent] revenue went up 3.7% a year while operating costs rose a little over 4% a year in King County. It’s never great when costs climb faster than revenue.

What Scott’s numbers show is that rent is tracking up, and it changes, going up and down over the years too. But the average rents are not climbing much faster than inflation and they are consistent in their climb; rents, in general, are not a volatile price.

But you have to keep in mind that costs to operate apartments are going up as well. According to Scott,

In 2012, taxes and utilities consumed 43% of total operating costs. Ten years from now they would consume 50% of total operating costs. After that, taxes and utilities continue to eat up a larger share of total operating costs every year.

So the gap between being rent revenue positive and breaking even is closing every month. That means at the current rate, without something changing, those lines will cross, and costs will exceed rent revenue. When I shared this fact on Twitter, Dominic Holden of the Stranger, Tweeted back, “Cry me a f….n’ river.”

Holden was expressing the dominant narrative that landlords have oodles of money and can afford reductions in rent revenue (he was also referencing an important American standard). But the idea that being a landlord means jacking up rents isn’t consistent with the data. In fact, market conditions being what they are have kept rents from increasing at the same rate as operating expenses. When you put that pressure on rents together with dwindling supply you have a recipe for inflation in the housing market.

All of this taken together means that rent is not rising too much higher than inflation. While one time rent increases are painful, in general they don’t happen every month or every year. When increases are averaged out over time they are about 3 to 5 percent, while general inflation is about 3 percent.

However, the costs to operate housing–especially utilities and taxes–are rising faster than rents over all, putting more pressure on rents. Add scarcity created by lower supply and increasing demand and the stage is set for rents climbing even faster and more frequently. That’s bad for landlords, but even worse for renters.

Then why not cap increases? Why not just impose controls on rents? Rent control makes no sense because the costs to operate will still keep rising. And if we don’t build more housing or make if we make it more difficult to, price pressures will increase. Even if every unit in the city is controlled, the point will come when hard expenses will simply exceed rents. Investors won’t build housing because they would get any return — they’d actually lose money.

Rent control would have to have cost controls too, which means wage freezes and freezes on tax collections and utility payments. Operating a multifamily apartment building isn’t free, and the expenses paid for taxes, insurance, maintenance, and an array of other fixed and unfixed costs for services can only be paid with rent revenue. And there are people who make their wages providing those services; do we expect them to take a pay cut too?

This is why rent control is folly. If we build more housing, we force competition between landlords to entice renters to sign a longer lease with a free month of rent; we can also eliminate the rules and limits that make it difficult to operate a rental property. We can can also expand the the Multifamily Tax Exemption (MFTE) Program which had demonstrated success. This is how we eliminate the pressures on price created by scarcity and rising costs. That’s why we need more housing and more choices, not mandates and controls.