TIFsplainer: Can We Use TIF to Build Housing on City Owned Land?

This post was written very quickly and mostly from memory. If you google my name and Tax Increment Financing, you’ll find a ton of stuff about many different aspects of this. But I wanted to get this all out even with some imperfections to get the conversation going. I’d suggest that along side this post you have the Municipal Research and Services Center (MRSC)’s rundown on property taxes in Washington State. Their resource overrides any errors I may have made below.

I think one big idea was left off the table from the Mayor’s Housing Affordability and Livability Agenda (HALA) Committee recommendations: Tax Increment Financing (TIF). I think it makes sense that this important financing tool has sort of disappeared. I was a big champion of the idea and even I am just coming back to it now after championing it for more than a decade. But I think that the TIF concept needs to be reintroduced into the discussion of how we finance public housing – that is housing that is owned and operated by local government. It’s going to take a lot of words and some pictures to do this, but let’s get started.

What is Tax Increment Financing?

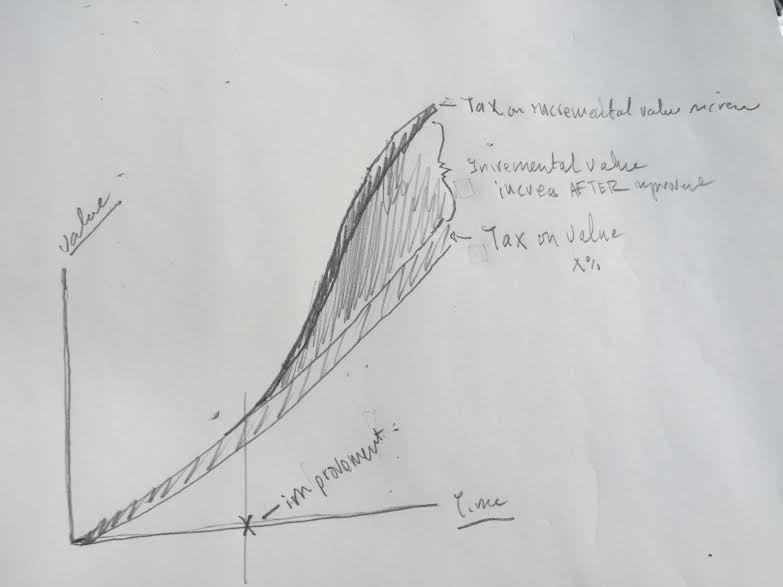

Tax Increment Financing or TIF is a value capture tool that enables local governments to borrow money by selling bonds, use the money to make improvements to infrastructure, and pay the money back by taxing a portion of the increases in property value created by the improvements.

It sounds more complicated than it really is. Imagine if you owned a piece of property with no road, sewer, or water service. That property would be worth a lot more with that infrastructure and would pay more property taxes. What TIF does is borrow money to build that infrastructure then, when the value of the property goes up, pay back the money with the extra taxes it collects. It’s called value capture because the using future increase in property value is what allows improvements today; that increment of increase value is the “I” in TIF.

Greatest diagram in the world courtesy of me.

The key ingredients for successful TIF are time, low interest loans from investors on the bond market and the value from improvements to infrastructure, and investment in the properties that benefit from the infrastructure. Ideally, the pay back of the borrowed money tracks well with tax revenue drawn from the benefitting parcels of land. The reason TIF makes sense for local governments is that it allows them to entice new housing and commercial development where no private investment wants to go because the costs of infrastructure are too high to offset with the revenue from what can be built.

Think about that parcel you own with no road, sewer, or water. If you wanted to sell it to a developer to build housing, she likely wouldn’t want to buy it, no matter what the zoning was because what she could charge for rents or for selling a house wouldn’t pay her back for the road, sewer, and water connections she’d have to build. You could build those things, but who’d loan you the money. What TIF does is allow the breaking of that cycle which results in higher tax revenue to cover the improvements, but also jobs, more housing and retail, and more sales tax.

Why Don’t We Use TIF in Seattle?

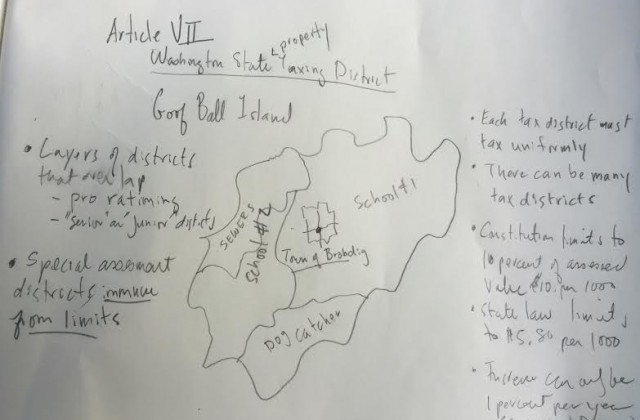

Washington State has a peculiar property tax code. The founders of the State worried that some property owners would be unfairly targeted with higher taxes. So they designed a Constitution that required uniform taxation. But they were smart enough to balance that out with creating tax districts. So while the State, counties, and cities are all taxing districts, there are a myriad of other special purpose taxing districts too. The only rule they have to follow set by the Constitution is that they tax no more than 1 percent of the value of the property and that taxes be uniform across all value in the district.

What makes our system counter intuitive is that we don’t assess property taxes on the value of particular property; instead we assess a rate of taxation of the total value of all property in a tax district and apply it across all the value. So if a tax district assesses a 1 percent tax on all property, it starts with the total value in the district. If the total value is $1,000,000 then it will collect $10,000. To make sure the tax is uniform, the local government has to divide that tax by the total value.

$10,000/$1,000,000 = $.01

Then the jurisdiction multiplies that number by $1000

$1000 x $.01 = $10

So if there are four property owners in the jurisdiction with properties valued at $250,000, $500,000, $100,000 and $150,000 each they’d pay,

$250,000 $2,500

$500,000 $5,000

$100,000 $1,000

$150,000 $1,500

$1,000,000 Total Value $10,000 Tax Collected (tax rate $.01/$1000)

You might look at this and say, “What’s your point? You just came up with a convoluted way of assessing a 1 percent property tax. You don’t need all that. Just do this:

$1,000,000 x .01 = $10,000

Each property gets assessed a simple bill of 1 percent. But the difference in Washington is that we don’t assess property taxes on the value of the specific property. It’s clearer when we mess with the value of one of the properties. Let’s say the first property on our list builds a new septic system. Her property value increases by $50,000.

$300,000 $2,857

$500,000 $4,750

$100,000 $ 950

$150,000 $1,425

$1,050,000 Total Value $10,000 Tax Collected (tax rate $.0095/$1000)

In a system where property taxes were applied by value of the property, what’s called ad valorem, the owner would pay $3,000 in taxes. In Washington, she pays $2,857.

You can see why this system foils TIF. If the local government pays for the septic system in hopes it would spur development, there is no incremental increase in taxes over time to pay back any debt incurred.

Remember two of the key ingredients needed for TIF are time and increased value. Those two elements create incremental increases in value that in ad valorem system (where a tax is applied as a percentage to a specific property). In Washington State, however, improvements that benefit a specific property or set of properties don’t result in a higher tax rate – in fact, it’s just the opposite, tax rates on the improved property can go down.

Statutory Limits on Property Taxes

So along with the Constitutional limits of 1 percent tax on value and uniformity, legislatures over the years have imposed limits that have lowered tax districts from collecting property taxes along with exemptions. For our purposes, the key things to keep in mind are the following legislatively imposed limits:

- State law has lowered the 1 percent allowed in the Constitution to .58 percent, or $5.80 per $1,000 or value rather than the constitutionally allowed $10;

- Since there are layers of taxing districts (State, County, City, School, etc.), it has designated senior and junior taxing districts;

- As properties in overlapping districts hit the $5.80 limit, junior taxing districts (schools for example) must share tax revenue through pro-rationing, taking a smaller share of property taxes;

- The Legislature passed a limit that local jurisdictions cannot increase their property taxes more than 1 percent from their previous year’s collection; and

- Some special assessment districts are immune from the $5.80 requirements (e.g. Transportation Districts)

What these limits do is make it increasingly challenging for the many overlapping taxing districts to collect taxes locally. And in Washington State, this tends to put more pressure on sales tax as an alternative to collect taxes for various projects or investments.

Further complicating this are State limits to what local governments can borrow on the bond market. Legislators in Olympia have set prescriptions for just how much any local government can borrow. As we discussed earlier, taxes are the revenue which breath confidence into lenders consideration of risk; when State government limits how much local government can tax and borrow it means fewer options for capital investment in infrastructure.

How Do We Get Real TIF?

The best way to fix all these problems and unleash real value capture using TIF would be to amend the State Constitution. The amendment would be rather straightforward, fixing Article VII to allow an exemption from uniformity for TIF districts. The establishment of those districts could be by popular vote, vote of property owners that would be subject to TIF assessments, or by the local government.

The proposal I supported several years ago would have allowed local governments to create a TIF taxing district and would have allowed an assessment based on the value of properties in the district for a set period of time, specifically the life of the bonds. It would have also created an exemption from the debt limits so that local government could go to the bond market without jeopardizing other borrowing.

The elegance of this solution is pretty impressive. Amending the Constitution in this way would allow pure TIF, something even Oregon lacks. In Oregon, the TIF district actually captures incremental value under their property tax limits that would otherwise belong to other taxing districts like schools. In Oregon the argument that TIF steals from schools to pay for infrastructure isn’t that far off since strong limits have been established for how much property would be taxed. Without going into Oregon’s tax system (don’t dare me!), TIF does create value there but TIF districts actually reduce tax revenue for other local governments.

An amendment to our Constitution creating ad valorem districts would mean that my silly diagram would be exactly how TIF would work. The City of Seattle could go to newly annexed White Center, draw a TIF district, borrow and spend $100 million on improvements to infrastructure, then as the property values on those properties in the districts went up over time (remember time?), the City could tax a percentage of that increase without worry about uniformity or the $5.80 limit. When the bonds for the infrastructure were paid off, the TIF district would disappear.

One of the biggest complaints I hear from our builders is lack of infrastructure; they either pay for it passing on the costs in the form of higher prices, or they don’t buy and build on properties that are otherwise zoned for lots of housing. That’s a bad outcome because it means less housing and higher prices. A TIF carve out in the Constitution would mean Seattle could invest in infrastructure and not have to take money away from schools or other priorities while lowering barriers on may hard to build on lots in Seattle.

How About Fake TIF?

The Mayor and Council and their staff are remarkable for their ability to make things up. For example, under any other circumstances they’d recognize that Mandatory Inclusionary Zoning is a really bad idea. But because it makes political sense, they all grind ahead and over all the numbers and doubts that suggest that while it would create some rent restricted units, it would do so by increasing over all housing prices.

They also have no problem making a deal with a rich dude who wants a basketball team.

The Mayor and Council have agreed in principle with the idea that they would go to the bond market, borrow money, build a stadium, and get paid back by the rich dude when the team (hockey or basketball) starts to make money and generating sales and B & O taxes.

What’s amusing or annoying, is that this “deal” didn’t require any kind of taxing district; it was just more or less a handshake deal. We build thus and such with borrowed money, you provide the team (or whatever), you sell tickets, and then you pay off the credit card bill every month. The City enjoys a team playing some kind of sports, gets sales tax revenue, and has the loan it took for the arena or stadium or whatever, paid for by the rich dude’s team.

You think I’m kidding. That’s exactly what they agreed to do.

Can’t we do the same kind of thing for housing on City owned land.

Get It Done!

It’s pretty simple really. Get some developers both public and private together and put together a plan for 500 units of housing (or more) at the soon to be decommissioned Roosevelt Reservoir. Get them and their investors, including Low Income Housing Tax Credit (LIHTC) investors and City Housing Levy money, to put down some money, issue some General Obligation Bonds, and build the housing at the Reservoir site.

The property would increase in value, the mixed market-rate and subsidized housing would produce revenue, you’d pay off the bonds, and there you have it. The value is captured not for a stadium but for a lot of housing and all without penalties or vilifying anyone. And the worse case scenario? The whole thing goes bust and everyone loses money. But guess what? We still have 500 units of housing!

There is simply no substantive difference between what the City agreed to do to try and lure an NBA team to Seattle and what it would take to build a lot of housing on City owned land. None. The only difference is motivation and politics. Our elected officials can’t see beyond the ends of their own noses. They have the power to do lots of amazing things with financing – if they want to.

Why TIF and Why Now?

Getting a constitutional amendment passed is almost impossible. But apparently so is getting the City Council and Mayor to think outside their narrow ideological box. I wrote all this because it feels good. I guess it’s therapeutic. And because I figure maybe, like a message in a bottle, someone might rescue us from this island where we’d rather pit renter against renter to battle over scarce housing in the name of social justice and preservation than build more; and island where we’d borrow money to build a facility for a basketball team that may or may not ever appear rather than do the same to build more housing.

{kind=link}