For Candidates: What’s Wrong With Seattle’s Mandatory Housing Affordability Program?

We’ve been working on a concise, one page description for candidates about why the City’s headlong rush into the disastrous policy of Mandatory Inclusionary Zoning (MIZ) is, well, disastrous. I still hear candidates calling the Grand Bargain, “HALA” and talking bout upzones associated with MIZ as “HALA” or “I support HALA,” or “I oppose HALA” etc. And on the Dori Monson show the other day I had to call out Councilmember Sawant who was suggesting that the upzones being passed should come with fees for developers. Ummm, well, they do. That’s what you voted for. Ignorance is a dangerous thing. Here’s yet another attempt to put it together.

Background: The Mandatory Housing Affordability (MHA) program is a form of Mandatory Inclusionary Zoning (MIZ), a change to the land use code that requires all new development to include rent restricted housing or pay a fee in lieu of that inclusion along with small increases in height. Seattle’s program was created as part of negotiations between a few larger market rate developers, non-profit developers (who get the fees), and representatives of the City of Seattle.

We weren’t invited: Representatives of the wider development community were left out of the process of negotiating the specifics of the MHA program. The builders of the vast majority of Seattle’s housing were not consulted on how the program would affect their projects.

Infeasible: The problem with MHA is that it adds cost to the building of new housing either through the loss of rent revenue from inclusion or from having to pay the fee. Also, building higher costs more, and those costs along with fees and inclusion are usually not offset by the additional floor area, making the project infeasible for financing.

Inflationary: When a project does work under MHA, it will be because the price of the product, housing, has to go up to compensate for the extra costs. This means higher rents or sales price to cover the costs of inclusion or paying the fee and the extra construction costs from building more floor area. Across the housing market, this means higher prices for people looking for housing.

Illegal: Analysis by the Pacific Legal Foundation indicates that MHA is essentially a forced auction of higher density zoning, and the requirement to buy something that adds unwanted costs is a violation of the Constitution and State law (RCW 82.02.020) that prohibits the taxation of development either directly or through mandates.

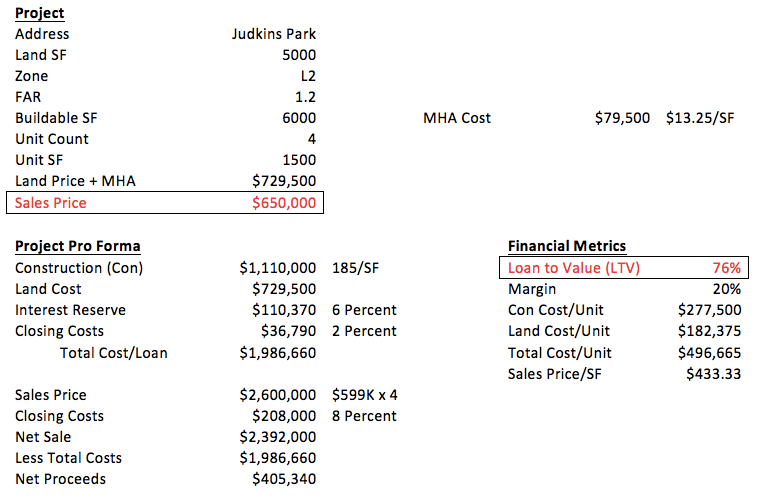

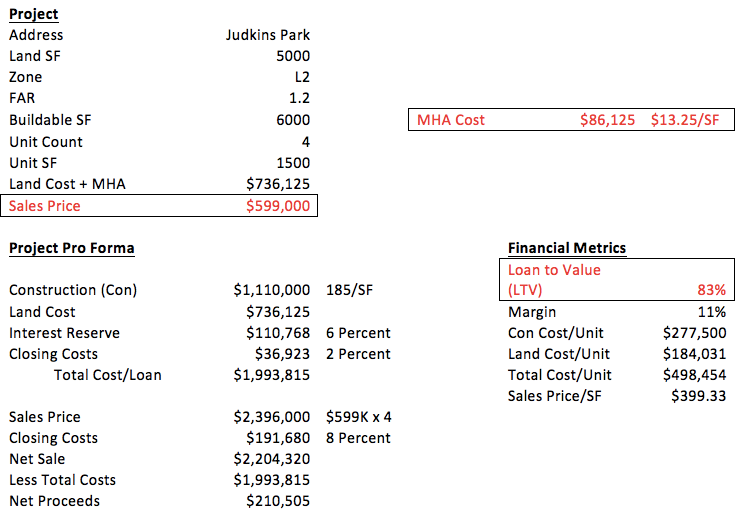

Case study: We looked at a typical 4 townhouse project, and when fees are imposed, the additional costs mean a higher loan to value ratio (LTV). The LTV is an index for lenders; when it gets above 80 percent, a project can’t get financing. In this example, the only way to lower the LTV was to raise the price of the houses from $599,000 to $650,000, an almost 10 percent increase in price. Apartment rents would go up in the same way.

What MIZ/MHA Does to LTV

Correcting MIZ/MHA Impact on LTV With A Higher Price