Hide and Seek: City’s Consultant Warns Don’t Interpret Residual Land Value “Literally”

The City has stubbornly resisted telling anyone how they intend to implement their version of Mandatory Inclusionary Zoning (MIZ), something they call Mandatory Housing Affordability – Residential (MHA). Some of the furtiveness comes from the fact that City staff are truly making stuff up as they go using guesses and back of the envelope assessments. But last week they finally have revealed the basis upon which they are determining (to their own satisfaction of course) whether their program is feasible. The methodology they are using is called Residual Land Value (RLV) and is almost universally rejected by most who actually build housing as a gauge of financial feasibility (something you’ll later see the consultants agree with). There hasn’t been time to rake through all the numbers, but we can discuss the RLV methodology and why it doesn’t have much use determining feasibility, but does validate the City’s agenda.

The report that I’ll be referring to is the HALA Economic Analysis Summary Memorandum produced by Community Attributes Inc., a company hired by the City. The memo was “requested an economic analysis that evaluates the economic viability of new development with the zoning changes and proposed payment or performance requirements associated with MHA.”

Essentially the memo is supposed to answer the question, “Will MHA work?” Put another way, it would appear to take the questions and objections we have seriously, that inclusion and fees associated with MHA would add costs to projects that would tip them into infeasibility. The question about the impacts of MHA comes from professionals that build housing because they know that the key to getting their projects completed is financing. Every project in town, with very few exceptions, is built with borrowed money. The worry about additional costs has nothing to do with loss of profits but pushing up the cost side to the point where price has to go up, and if prices go up beyond what the market will bear, lenders and investors won’t put their money into a project. I explained this at length in a post about a 4-unit townhouse project. I’ll use that same project here to take a look at RLV.

First, what is RLV and how is it calculated? I’ll use the simple explanation from the memo of how RLV is calculated.

The formula for determining residual land value is: Project value minus costs minus return = RLV.

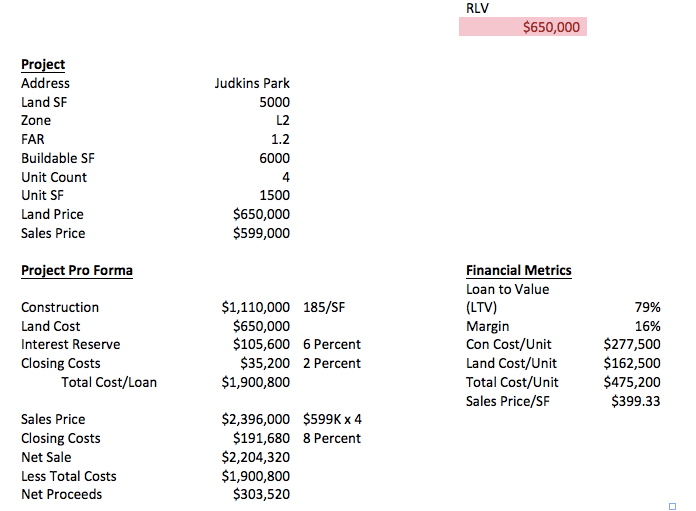

Here’s how RLV looks when calculated on our Judkins Park project:

You’ll see everything is pretty much the same and the sales price of the land is the same as the calculated RLV. This is because the RLV calculation just isolates what’s left over for land when all other expenses and the margin are accounted for from the sales price. Someone could do the same calculation for Residual Construction Value and that would be the same as the construction total. We’ll see how RLV is being used when we look at our AFTER pro forma.

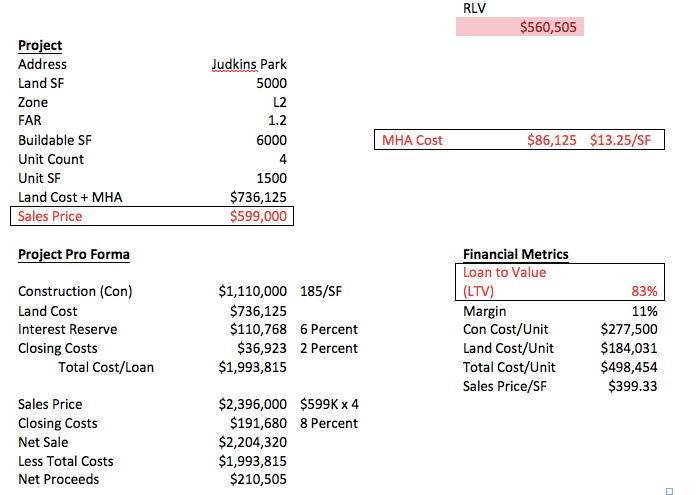

Now, you can see that after the fee is put into the mix, the RLV goes down by about $90,000. Unless some other input changes, our builder won’t have enough money to make the project work. The RLV calculation shows that the fee makes this project infeasible. What if we raise the sales price?

Now, you can see that after the fee is put into the mix, the RLV goes down by about $90,000. Unless some other input changes, our builder won’t have enough money to make the project work. The RLV calculation shows that the fee makes this project infeasible. What if we raise the sales price?

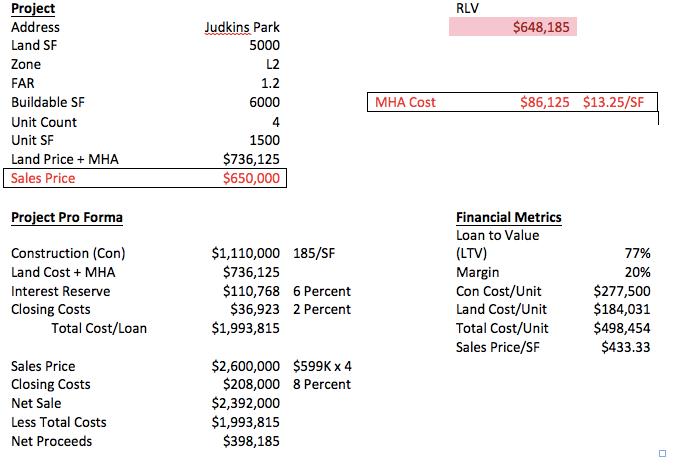

Now the project “works” because the higher sales price has absorbed the fee. The RLV number is just about the asking price of $650,000. But as we’ve pointed out over and over, it makes no sense to squeeze money out of market rate projects in the name of making housing affordable; this won’t happen. Instead the fees will end up just raising housing prices to absorb the extra costs.

The RLV formula is logical. If you were standing on the sidewalk in front of a vacant lot with a “For Sale” sign you could do the math in your head. If I take the cost of construction, financing, and return from the sale of the property and subtract all that from what I could sell four townhomes on the lot, you’d get a number. In theory, that number is what you should or can pay for the land. The price of land is an important component in determining the financial feasibility of a project. But using RLV has its limits.

And no, the fee can’t just “come out of the profits.” Remember the Loan To Value (LTV) ratio? The lender and the investor need that number to be 75 percent or lower. They won’t accept a lower ratio that would result from lowering the margin.

And no, the seller won’t just lower the price of the land $90,000. There isn’t any reason the builder couldn’t or wouldn’t point out the fee before she bought the land, but prices for housing climbing the seller might just put the house that is on the lot for sale as is. Or he might just hold out waiting for someone else who will have a lender willing to boost the price of the townhomes.

The memo issued by the consultant is very accurate and matter of fact about the usefulness of RLV to help understand the impact of the MHA fees and costs of inclusion. But RLV might establish some broad measure of impact on what builders can pay for land after MHA, it doesn’t consider financing requirements or other costs that arise during development like:

- Power line setbacks

- Water/sewer main extensions

- Effective townhome unit width minimums (market driven, not building or LU code)

- Dilution of value for each added floor (i.e. a 3 story 1,400 sf townhome is more valuable than a 4 story 1,400 sf townhome)

And the consultants agree. Here’s what they say, emphasis is mine:

Because of the uncertainty that comes with the hypothetical developments modeled in this analysis, one must take care to not interpret residual land value literally for willingness-to-pay for land. Many other site-specific factors come into play for true willingness-to-play, such as opportunity costs of putting that investment toward other sites that might be more attractive (Page 4).

There has been a stubborn insistence among some advocates and supporters of MIZ generally and MHA in particular that the fees and inclusion will get paid for “out of the land.” That is, when the fees and inclusionary requirements get high enough, land prices will go down exactly in the amount of the fees or lost rent revenue. This view of real estate is what enables some people to support MIZ with a straight face. Prices won’t go up and nobody will lose money but the person who is selling land, and who cares about them anyway, they were just speculating. But even the City’s consultants in the paragraph I just quoted are smart enough to allow for wide variance for “willingness to play,” or pay.

What everyone must understand about MHA is that it won’t lower housing prices it will increase overall housing prices. The consultant is just handing over data. But they acknowledge that data and analysis doesn’t consider financing, the essential ingredient of any housing project (see above). The City has just shrugged and figured either the new homeowner will pay or the landowner will pay. As long as non-profit developers get their pay day, who cares? I’ll close by quoting a paragraph (emphasis mine) the City should listen to but likely won’t.

RLV models provide enough detail and structure to understand major cost and revenue drivers and, because they rely on local market data, they effectively convey information about the types of projects that are more or less feasible in a given area. They also provide an avenue to evaluate and compare feasibility efficiently and across a large number of development typologies and zones. An alternative method is a pro forma cash flow model, which incorporates more detailed financial metrics and investment criteria. When underwriting a specific development, a developer will use a cash flow model to gain an in-depth understanding of the financial performance of a development project. Detailed cash flow models are not necessary, nor particularly well-suited, to answer policy questions at this scale and altitude because they require very detailed assumptions that are likely to be highly variable across different development projects. (Page 4)

Featured image is Hiding in the Haycocks, painted in 1881 by William Bliss Baker.